Curve Fitting and Regression#

In this lecture, we’ll learn how to find the best mathematical function to describe noisy experimental data.

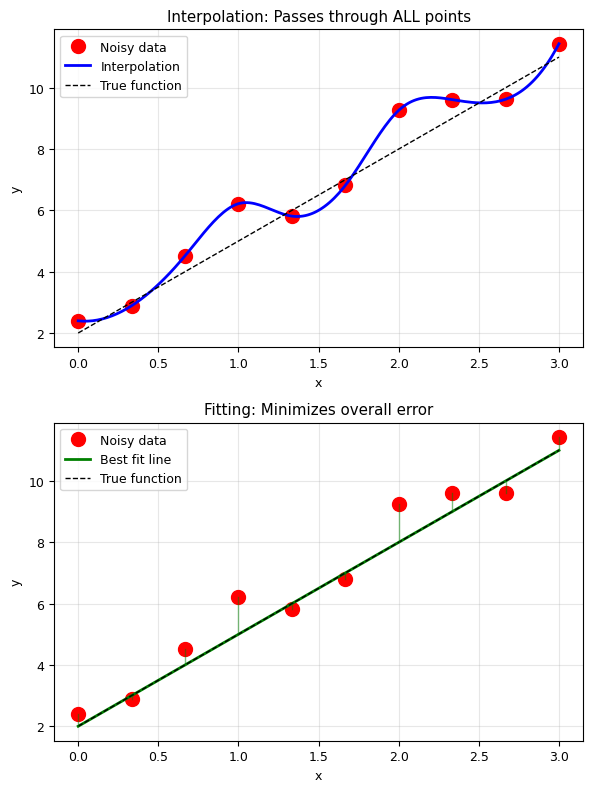

Fitting vs. Interpolation#

Interpolation |

Curve Fitting |

|---|---|

Passes through ALL points |

Finds the best overall trend |

Assumes data is exact |

Accounts for noise and errors |

Can oscillate wildly |

Smoother, more robust |

Good for tabulated data |

Good for experimental data |

import numpy as np

import matplotlib.pyplot as plt

# For nicer plots

plt.rcParams['figure.figsize'] = [6, 4]

plt.rcParams['font.size'] = 9

I. The Fitting Problem#

Given noisy data points \((x_1, y_1), (x_2, y_2), \ldots, (x_n, y_n)\), we want to find a function \(f(x)\) that best describes the underlying trend.

Unlike interpolation, the function does NOT need to pass through the data points. Instead, we minimize the overall error between the model and the data.

# Visualize the difference between interpolation and fitting

from scipy.interpolate import interp1d

# True underlying function

f_true = lambda x: 3*x + 2

# Generate noisy data

np.random.seed(42)

x_data = np.linspace(0, 3, 10)

y_data = f_true(x_data) + np.random.randn(10) * 0.8

# Interpolation (passes through all points)

f_interp = interp1d(x_data, y_data, kind='cubic')

x_fine = np.linspace(0, 3, 200)

plt.figure(figsize=(6, 8))

plt.subplot(2, 1, 1)

plt.plot(x_data, y_data, 'ro', markersize=10, label='Noisy data')

plt.plot(x_fine, f_interp(x_fine), 'b-', linewidth=2, label='Interpolation')

plt.plot(x_fine, f_true(x_fine), 'k--', linewidth=1, label='True function')

plt.xlabel('x')

plt.ylabel('y')

plt.title('Interpolation: Passes through ALL points')

plt.legend()

plt.grid(True, alpha=0.3)

plt.subplot(2, 1, 2)

plt.plot(x_data, y_data, 'ro', markersize=10, label='Noisy data')

plt.plot(x_fine, f_true(x_fine), 'g-', linewidth=2, label='Best fit line')

plt.plot(x_fine, f_true(x_fine), 'k--', linewidth=1, label='True function')

# Show residuals

for i in range(len(x_data)):

plt.plot([x_data[i], x_data[i]], [y_data[i], f_true(x_data[i])],

'g-', alpha=0.5, linewidth=1)

plt.xlabel('x')

plt.ylabel('y')

plt.title('Fitting: Minimizes overall error')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print('Interpolation follows every bump in the noise.')

print('Fitting captures the TRUE underlying trend.')

Interpolation follows every bump in the noise.

Fitting captures the TRUE underlying trend.

II. The Least Squares Principle#

What is the “best” fit?#

We need a criterion. The most common is least squares: minimize the sum of squared residuals.

Given data \((x_i, y_i)\) and a model \(f(x)\), the error (or cost function) is:

The best fit is the one that minimizes this error.

Why squared differences?#

Positive and negative errors don’t cancel out

Larger errors are penalized more heavily

The math works out nicely (differentiable, has unique minimum)

Related to maximum likelihood estimation for Gaussian noise

III. Linear Fitting (from Scratch)#

The Simplest Case: \(f(x) = ax + b\)#

We want to find the slope \(a\) and intercept \(b\) that minimize:

Deriving the Solution#

At the minimum, the partial derivatives must be zero:

These give us a system of two linear equations:

Matrix Form#

This can be written as \(\mathbf{A} \vec{p} = \vec{c}\):

This is just solving \(\mathbf{A}\vec{p} = \vec{c}\)!

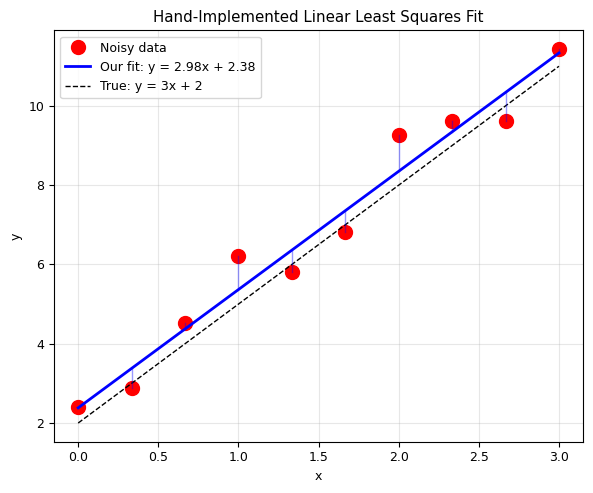

# Implement linear fitting from scratch

def linear_fit(x, y):

"""

Linear least squares fit: y = a*x + b

Implemented from scratch using the normal equations.

Parameters:

x, y: arrays of data points

Returns:

a (slope), b (intercept)

"""

n = len(x)

# Compute the sums we need

sum_x = np.sum(x)

sum_y = np.sum(y)

sum_x2 = np.sum(x**2)

sum_xy = np.sum(x*y)

# Build the matrix equation: A @ [b, a] = c

A = np.array([ [n, sum_x],

[sum_x, sum_x2]

])

c = np.array([sum_y, sum_xy])

# Solve A @ p = c

p = np.linalg.solve(A, c)

b, a = p # p = [b, a]

return a, b

# Test with our noisy data

a_fit, b_fit = linear_fit(x_data, y_data)

print(f'True parameters: a = 3.000, b = 2.000')

print(f'Fitted parameters: a = {a_fit:.3f}, b = {b_fit:.3f}')

# Plot

plt.figure(figsize=(6, 5))

plt.plot(x_data, y_data, 'ro', markersize=10, label='Noisy data')

plt.plot(x_fine, a_fit * x_fine + b_fit, 'b-', linewidth=2,

label=f'Our fit: y = {a_fit:.2f}x + {b_fit:.2f}')

plt.plot(x_fine, f_true(x_fine), 'k--', linewidth=1, label='True: y = 3x + 2')

# Show residuals

for i in range(len(x_data)):

y_pred = a_fit * x_data[i] + b_fit

plt.plot([x_data[i], x_data[i]], [y_data[i], y_pred],

'b-', alpha=0.4, linewidth=1)

plt.xlabel('x')

plt.ylabel('y')

plt.title('Hand-Implemented Linear Least Squares Fit')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

True parameters: a = 3.000, b = 2.000

Fitted parameters: a = 2.983, b = 2.383

Alternative: Using scipy.optimize.minimize#

We can also find the fit by directly minimizing the error function numerically:

# Method 2: Using scipy.optimize.minimize

from scipy.optimize import minimize

# Define the model function

def fit_func(x, a, b):

return a * x + b

# Define the error (cost) function

def err_func(params, x, y):

"""Sum of squared residuals."""

a, b = params

y_pred = fit_func(x, a, b)

err = np.sum((y - y_pred)**2)

return err

# Minimize!

param_init = [1.0, 1.0] # Initial guess

result = minimize(err_func, param_init, args=(x_data, y_data))

a_opt, b_opt = result.x

print(f'Our analytic solution: a = {a_fit:.4f}, b = {b_fit:.4f}')

print(f'scipy.optimize result: a = {a_opt:.4f}, b = {b_opt:.4f}')

print(f'\nThey match! Both methods give the same answer.')

print(f'\nMinimum error: {result.fun:.4f}')

print(f'Optimization converged: {result.success}')

Our analytic solution: a = 2.9834, b = 2.3833

scipy.optimize result: a = 2.9834, b = 2.3833

They match! Both methods give the same answer.

Minimum error: 3.0085

Optimization converged: True

IV. Polynomial Fitting#

Generalizing to Higher-Order Polynomials#

For a polynomial of degree \(j\): \(f(x) = a_0 + a_1 x + a_2 x^2 + \cdots + a_j x^j\)

The least squares condition leads to the normal equations in matrix form:

This is again \(\mathbf{A}\vec{p} = \vec{c}\), where \(\mathbf{A}\) is a (j+1) × (j+1) matrix.

Note#

The matrix \(\mathbf{A}\) is called the Vandermonde matrix and can become ill-conditioned for high polynomial degrees.

# Implement polynomial fitting from scratch

def poly_fit_manual(x, y, degree):

"""

Polynomial least squares fit - implemented from scratch.

Parameters:

x, y: arrays of data points

degree: degree of the polynomial

Returns:

coefficients [a0, a1, a2, ...]

"""

n = degree + 1 # Number of coefficients

# Build the normal equation matrix A

A = np.zeros((n, n))

for row in range(n):

for col in range(n):

# code..

# A[row, col] = ...

A[row, col] = np.sum(x**(row+col))

# Build the right-hand side vector c

c = np.zeros(n)

for row in range(n):

# code ..

# c[row] = ...

c[row] = np.sum(y*x**row)

# Solve for coefficients

coeffs = np.linalg.solve(A, c)

return coeffs # [a0, a1, a2, ...]

def poly_eval(coeffs, x):

"""Evaluate polynomial given coefficients [a0, a1, a2, ...]."""

result = np.zeros_like(x, dtype=float)

for i, a in enumerate(coeffs):

result += a * x**i

return result

# Generate quadratic data with noise

np.random.seed(42)

x_poly = np.linspace(0, 10, 50)

y_poly = 2*x_poly**2 + 3*x_poly + 4 + np.random.normal(0, 10, 50)

# Fit with our hand-implemented function

coeffs = poly_fit_manual(x_poly, y_poly, 2)

print(f'True coefficients: a0 = 4, a1 = 3, a2 = 2')

print(f'Fitted coefficients: a0 = {coeffs[0]:.2f}, a1 = {coeffs[1]:.2f}, a2 = {coeffs[2]:.2f}')

# Plot

x_plot = np.linspace(0, 10, 200)

plt.figure(figsize=(6, 5))

plt.plot(x_poly, y_poly, 'ro', markersize=5, alpha=0.6, label='Noisy data')

plt.plot(x_plot, poly_eval(coeffs, x_plot), 'b-', linewidth=2,

label=f'Our fit: {coeffs[2]:.1f}x² + {coeffs[1]:.1f}x + {coeffs[0]:.1f}')

plt.plot(x_plot, 2*x_plot**2 + 3*x_plot + 4, 'k--', linewidth=1,

label='True: 2x² + 3x + 4')

plt.xlabel('x')

plt.ylabel('y')

plt.title('Hand-Implemented Polynomial Fitting (Degree 2)')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

True coefficients: a0 = 4, a1 = 3, a2 = 2

Fitted coefficients: a0 = 8.14, a1 = 0.28, a2 = 2.21

Using np.polyfit from NumPy#

NumPy provides np.polyfit(x, y, degree) for polynomial fitting, and np.polyval(p, x) for evaluation.

# Compare our result with numpy's polyfit

p_numpy = np.polyfit(x_poly, y_poly, 2) # Returns [a2, a1, a0] (highest first!)

print('Our implementation: a0={:.2f}, a1={:.2f}, a2={:.2f}'.format(*coeffs))

print('np.polyfit: a0={:.2f}, a1={:.2f}, a2={:.2f}'.format(p_numpy[2], p_numpy[1], p_numpy[0]))

print('\nNote: np.polyfit returns coefficients in REVERSE order (highest degree first)!')

Our implementation: a0=8.14, a1=0.28, a2=2.21

np.polyfit: a0=8.14, a1=0.28, a2=2.21

Note: np.polyfit returns coefficients in REVERSE order (highest degree first)!

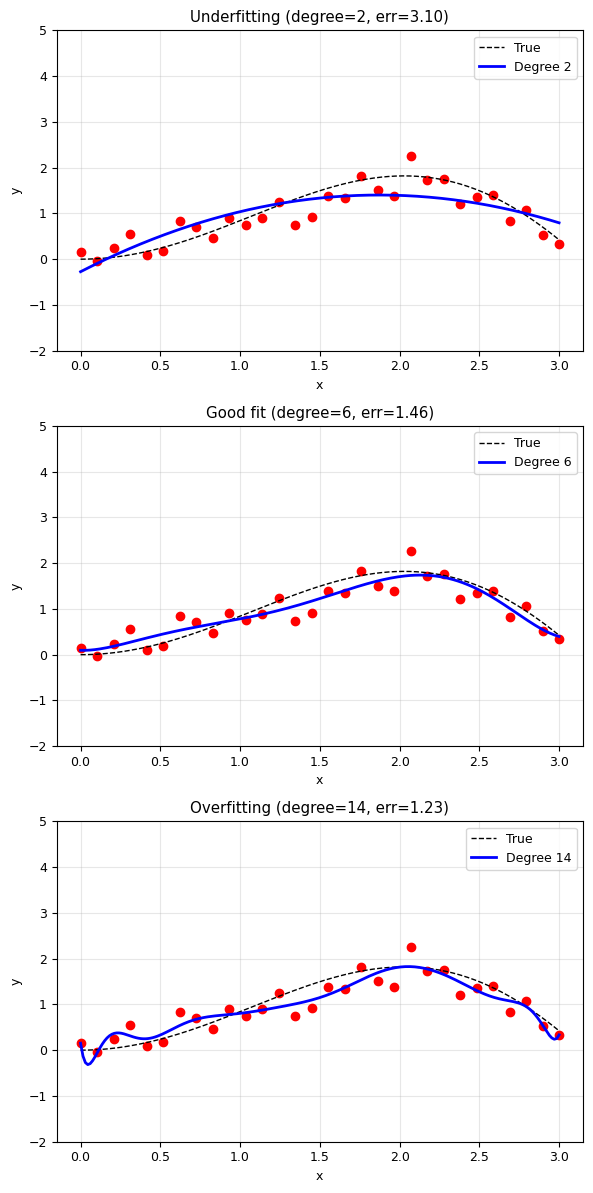

Choosing the Right Polynomial Degree#

Quiz: Try different polynomial degrees. Which one gives the best fit?

# Effect of polynomial degree: underfitting vs overfitting

f_complex = lambda x: x * np.sin(x)

np.random.seed(42)

x_demo = np.linspace(0, 3, 30)

y_demo = f_complex(x_demo) + 0.3 * np.random.randn(30)

x_fine_demo = np.linspace(0, 3, 200)

plt.figure(figsize=(6, 12))

for idx, order in enumerate([2, 6, 14]):

plt.subplot(3, 1, idx + 1)

fit = np.polyfit(x_demo, y_demo, order)

y_pred = np.polyval(fit, x_fine_demo)

# Compute residual

y_pred_data = np.polyval(fit, x_demo)

residual = np.sum((y_demo - y_pred_data)**2)

plt.plot(x_demo, y_demo, 'ro', markersize=6)

plt.plot(x_fine_demo, f_complex(x_fine_demo), 'k--', linewidth=1, label='True')

plt.plot(x_fine_demo, y_pred, 'b-', linewidth=2, label=f'Degree {order}')

plt.xlabel('x')

plt.ylabel('y')

title = ['Underfitting', 'Good fit', 'Overfitting'][idx]

plt.title(f'{title} (degree={order}, err={residual:.2f})')

plt.legend()

plt.grid(True, alpha=0.3)

plt.ylim(-2, 5)

plt.tight_layout()

plt.show()

print('Underfitting: Model too simple — misses the trend')

print('Overfitting: Model too complex — fits the noise, not the signal')

print('Good fit: Right balance — captures the trend, ignores the noise')

Underfitting: Model too simple — misses the trend

Overfitting: Model too complex — fits the noise, not the signal

Good fit: Right balance — captures the trend, ignores the noise

V. General Curve Fitting#

What if the model is not a polynomial? For example:

Exponential decay: \(f(x) = a \, e^{-bx} + c\)

Gaussian: \(f(x) = \frac{1}{\sqrt{2\pi\sigma^2}} e^{-(x-\mu)^2/(2\sigma^2)}\)

Power law: \(f(x) = a \, x^b\)

Sinusoidal: \(f(x) = A \sin(\omega x + \phi)\)

Two Approaches#

scipy.optimize.minimize— Define an error function and minimize it (we already know this!)scipy.optimize.curve_fit— A convenient wrapper designed specifically for fitting

Method 1: Using scipy.optimize.minimize (by hand)#

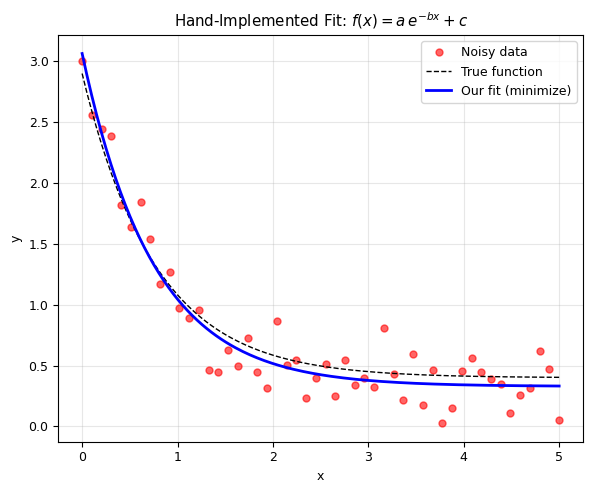

# Example: Fit an exponential decay f(x) = a * exp(-b*x) + c

from scipy.optimize import minimize

# Generate data

np.random.seed(42)

a_true, b_true, c_true = 2.5, 1.3, 0.4

x_exp = np.linspace(0, 5, 50)

y_exp = a_true * np.exp(-b_true * x_exp) + c_true + 0.2 * np.random.randn(50)

# Step 1: Define the model function

def exp_model(x, a, b, c):

return a * np.exp(-b * x) + c

# Step 2: Define the error function

def err_exp(params, x, y):

a, b, c = params

y_pred = exp_model(x, a, b, c)

return np.sum((y - y_pred)**2)

# Step 3: Minimize!

param_init = [1.0, 1.0, 0.0] # Initial guess

result = minimize(err_exp, param_init, args=(x_exp, y_exp))

a_fit, b_fit, c_fit = result.x

print('True parameters: a={:.3f}, b={:.3f}, c={:.3f}'.format(a_true, b_true, c_true))

print('Fitted parameters: a={:.3f}, b={:.3f}, c={:.3f}'.format(a_fit, b_fit, c_fit))

# Plot

x_plot = np.linspace(0, 5, 200)

plt.figure(figsize=(6, 5))

plt.plot(x_exp, y_exp, 'ro', markersize=5, alpha=0.6, label='Noisy data')

plt.plot(x_plot, exp_model(x_plot, a_true, b_true, c_true), 'k--', linewidth=1, label='True function')

plt.plot(x_plot, exp_model(x_plot, a_fit, b_fit, c_fit), 'b-', linewidth=2, label='Our fit (minimize)')

plt.xlabel('x')

plt.ylabel('y')

plt.title(r'Hand-Implemented Fit: $f(x) = a \, e^{-bx} + c$')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

True parameters: a=2.500, b=1.300, c=0.400

Fitted parameters: a=2.736, b=1.339, c=0.329

Method 2: Using scipy.optimize.curve_fit#

curve_fit is a convenient function designed specifically for fitting. It:

Takes the model function, x data, and y data

Returns optimal parameters AND their covariance matrix (uncertainty!)

from scipy.optimize import curve_fit

# curve_fit expects f(x, param1, param2, ...)

# It returns (optimal_params, covariance_matrix)

params_cf, covariance = curve_fit(exp_model, x_exp, y_exp, p0=[1, 1, 0])

# Extract parameter uncertainties from covariance matrix

uncertainties = np.sqrt(np.diag(covariance))

print('curve_fit results:')

print(f' a = {params_cf[0]:.4f} +/- {uncertainties[0]:.4f}')

print(f' b = {params_cf[1]:.4f} +/- {uncertainties[1]:.4f}')

print(f' c = {params_cf[2]:.4f} +/- {uncertainties[2]:.4f}')

print(f'\nTrue values: a={a_true}, b={b_true}, c={c_true}')

print('\nAdvantage of curve_fit: it gives you uncertainties automatically!')

curve_fit results:

a = 2.7355 +/- 0.1188

b = 1.3390 +/- 0.1132

c = 0.3289 +/- 0.0396

True values: a=2.5, b=1.3, c=0.4

Advantage of curve_fit: it gives you uncertainties automatically!

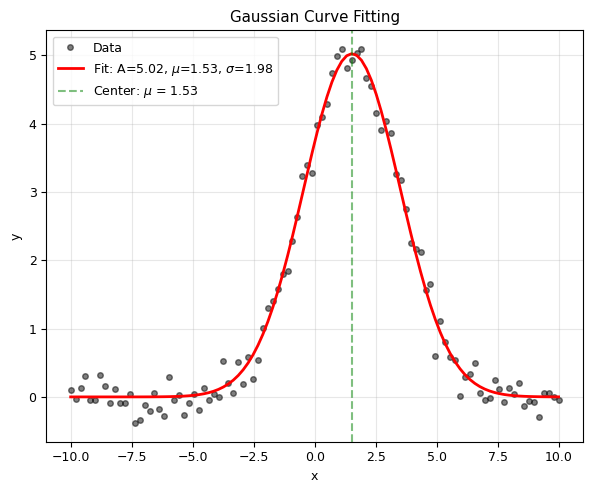

Example: Gaussian Fitting#

Fitting a Gaussian peak is very common in spectroscopy, particle physics, and signal processing.

# Gaussian fitting example

def gaussian(x, A, mu, sigma):

"""Gaussian function with amplitude A, center mu, width sigma."""

return A * np.exp(-(x - mu)**2 / (2 * sigma**2))

# Generate data

np.random.seed(42)

x_gauss = np.linspace(-10, 10, 100)

y_gauss = gaussian(x_gauss, 5.0, 1.5, 2.0) + 0.2 * np.random.randn(100)

# Fit

params_gauss, cov_gauss = curve_fit(gaussian, x_gauss, y_gauss, p0=[4, 0, 1])

A_fit, mu_fit, sigma_fit = params_gauss

errs = np.sqrt(np.diag(cov_gauss))

# Plot

plt.figure(figsize=(6, 5))

plt.plot(x_gauss, y_gauss, 'ko', markersize=4, alpha=0.5, label='Data')

plt.plot(x_gauss, gaussian(x_gauss, *params_gauss), 'r-', linewidth=2,

label=f'Fit: A={A_fit:.2f}, $\\mu$={mu_fit:.2f}, $\\sigma$={sigma_fit:.2f}')

plt.axvline(mu_fit, color='g', linestyle='--', alpha=0.5, label=f'Center: $\\mu$ = {mu_fit:.2f}')

plt.xlabel('x')

plt.ylabel('y')

plt.title('Gaussian Curve Fitting')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f'Fitted: A = {A_fit:.3f} +/- {errs[0]:.3f}')

print(f' mu = {mu_fit:.3f} +/- {errs[1]:.3f}')

print(f' sigma = {sigma_fit:.3f} +/- {errs[2]:.3f}')

print(f'True: A = 5.000, mu = 1.500, sigma = 2.000')

Fitted: A = 5.024 +/- 0.054

mu = 1.531 +/- 0.024

sigma = 1.980 +/- 0.024

True: A = 5.000, mu = 1.500, sigma = 2.000

VI. Goodness of Fit#

How do we know if our fit is good? Several metrics:

Residual Sum of Squares (RSS)#

Coefficient of Determination (\(R^2\))#

where TSS = Total Sum of Squares.

\(R^2 = 1\): Perfect fit

\(R^2 = 0\): Model no better than the mean

\(R^2 < 0\): Model is worse than the mean!

Reduced Chi-Squared (\(\chi^2_\nu\))#

where \(p\) = number of parameters, \(\sigma_i\) = measurement uncertainty.

\(\chi^2_\nu \approx 1\): Good fit

\(\chi^2_\nu \gg 1\): Poor fit (or underestimated uncertainties)

\(\chi^2_\nu \ll 1\): Overfitting (or overestimated uncertainties)

def compute_r_squared(y_data, y_pred):

"""Compute R² (coefficient of determination)."""

ss_res = np.sum((y_data - y_pred)**2) # Residual sum of squares

ss_tot = np.sum((y_data - np.mean(y_data))**2) # Total sum of squares

return 1 - ss_res / ss_tot

# Compare R² for different polynomial degrees

print('R² for different polynomial degrees:')

print('=' * 40)

for degree in range(1, 8):

p = np.polyfit(x_demo, y_demo, degree)

y_pred = np.polyval(p, x_demo)

r2 = compute_r_squared(y_demo, y_pred)

print(f' Degree {degree}: R² = {r2:.6f}')

print('\nNote: R² always increases with degree (more parameters)!')

print('But higher R² does NOT always mean a better model.')

print('Use adjusted R² or cross-validation to avoid overfitting.')

R² for different polynomial degrees:

========================================

Degree 1: R² = 0.315799

Degree 2: R² = 0.679083

Degree 3: R² = 0.827932

Degree 4: R² = 0.834795

Degree 5: R² = 0.841264

Degree 6: R² = 0.848789

Degree 7: R² = 0.852316

Note: R² always increases with degree (more parameters)!

But higher R² does NOT always mean a better model.

Use adjusted R² or cross-validation to avoid overfitting.

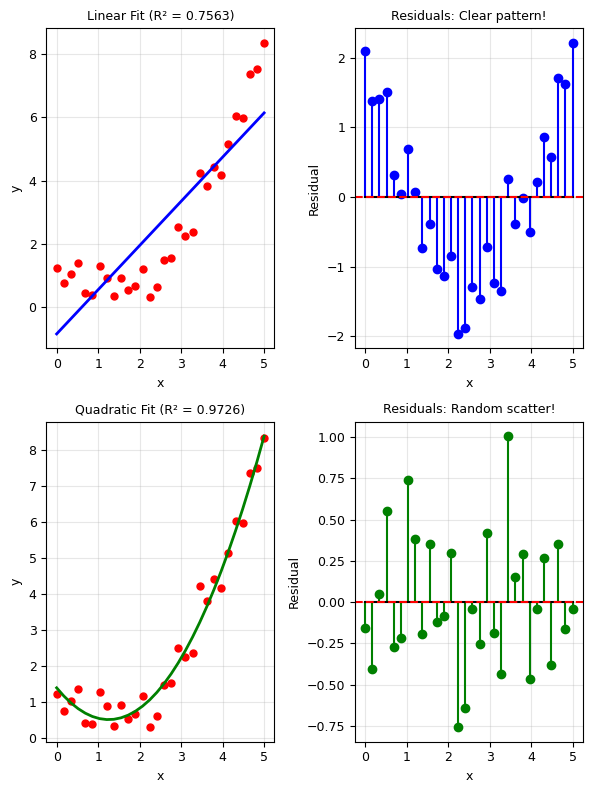

Residual Analysis#

A good fit should have random residuals. Patterns in residuals indicate a poor model.

# Residual analysis: linear vs quadratic fit on quadratic data

np.random.seed(42)

x_res = np.linspace(0, 5, 30)

y_res = 0.5 * x_res**2 - x_res + 1 + 0.5 * np.random.randn(30)

# Linear fit

p_lin = np.polyfit(x_res, y_res, 1)

residuals_lin = y_res - np.polyval(p_lin, x_res)

# Quadratic fit

p_quad = np.polyfit(x_res, y_res, 2)

residuals_quad = y_res - np.polyval(p_quad, x_res)

fig, axes = plt.subplots(2, 2, figsize=(6, 8))

# Linear fit

axes[0, 0].plot(x_res, y_res, 'ro', markersize=5)

axes[0, 0].plot(x_res, np.polyval(p_lin, x_res), 'b-', linewidth=2)

axes[0, 0].set_title(f'Linear Fit (R² = {compute_r_squared(y_res, np.polyval(p_lin, x_res)):.4f})', fontsize=9)

axes[0, 0].set_xlabel('x')

axes[0, 0].set_ylabel('y')

axes[0, 0].grid(True, alpha=0.3)

axes[0, 1].stem(x_res, residuals_lin, linefmt='b-', markerfmt='bo', basefmt='k-')

axes[0, 1].axhline(0, color='r', linestyle='--')

axes[0, 1].set_title('Residuals: Clear pattern!', fontsize=9)

axes[0, 1].set_xlabel('x')

axes[0, 1].set_ylabel('Residual')

axes[0, 1].grid(True, alpha=0.3)

# Quadratic fit

axes[1, 0].plot(x_res, y_res, 'ro', markersize=5)

axes[1, 0].plot(x_res, np.polyval(p_quad, x_res), 'g-', linewidth=2)

axes[1, 0].set_title(f'Quadratic Fit (R² = {compute_r_squared(y_res, np.polyval(p_quad, x_res)):.4f})', fontsize=9)

axes[1, 0].set_xlabel('x')

axes[1, 0].set_ylabel('y')

axes[1, 0].grid(True, alpha=0.3)

axes[1, 1].stem(x_res, residuals_quad, linefmt='g-', markerfmt='go', basefmt='k-')

axes[1, 1].axhline(0, color='r', linestyle='--')

axes[1, 1].set_title('Residuals: Random scatter!', fontsize=9)

axes[1, 1].set_xlabel('x')

axes[1, 1].set_ylabel('Residual')

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print('Linear fit: Residuals show a pattern -> wrong model!')

print('Quadratic fit: Residuals are random -> good model!')

Linear fit: Residuals show a pattern -> wrong model!

Quadratic fit: Residuals are random -> good model!

VII. Distance Metrics: Beyond Least Squares#

The least squares (\(L_2\) norm) is the most common, but not the only option:

\(L_p\) Distances#

Distance Metrics#

Distance |

Properties |

|---|---|

\(L_1\) (Manhattan) |

Robust to outliers |

\(L_2\) (Euclidean) |

Most common, smooth |

\(L_\infty\) (Chebyshev) |

Minimizes worst case |

\(L_1\) (Manhattan)

\(L_2\) (Euclidean)

$\(

\sqrt{\sum_i (y_i - f(x_i))^2}

\)$

\(L_\infty\) (Chebyshev)

When to use which?#

\(L_2\): Default choice, best for Gaussian noise

\(L_1\): When data has outliers (more robust)

\(L_\infty\): When worst-case error matters

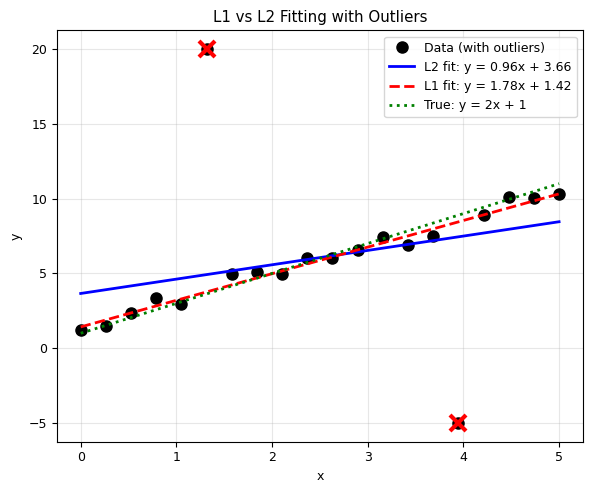

# Demonstrate L1 vs L2 with outliers

np.random.seed(42)

x_out = np.linspace(0, 5, 20)

y_out = 2 * x_out + 1 + 0.5 * np.random.randn(20)

# Add outliers

y_out[5] = 20 # Far from trend

y_out[15] = -5 # Far from trend

# L2 fit (standard least squares)

p_L2 = np.polyfit(x_out, y_out, 1)

# L1 fit (minimize absolute deviations)

def err_L1(params, x, y):

a, b = params

return np.sum(np.abs(y - (a * x + b)))

result_L1 = minimize(err_L1, [1, 1], args=(x_out, y_out), method='Nelder-Mead')

a_L1, b_L1 = result_L1.x

plt.figure(figsize=(6, 5))

plt.plot(x_out, y_out, 'ko', markersize=8, label='Data (with outliers)')

plt.plot(x_out[5], y_out[5], 'rx', markersize=12, markeredgewidth=3)

plt.plot(x_out[15], y_out[15], 'rx', markersize=12, markeredgewidth=3)

plt.plot(x_out, np.polyval(p_L2, x_out), 'b-', linewidth=2,

label=f'L2 fit: y = {p_L2[0]:.2f}x + {p_L2[1]:.2f}')

plt.plot(x_out, a_L1 * x_out + b_L1, 'r--', linewidth=2,

label=f'L1 fit: y = {a_L1:.2f}x + {b_L1:.2f}')

plt.plot(x_out, 2 * x_out + 1, 'g:', linewidth=2, label='True: y = 2x + 1')

plt.xlabel('x')

plt.ylabel('y')

plt.title('L1 vs L2 Fitting with Outliers')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print('L2 is pulled toward the outliers (sensitive to large errors).')

print('L1 is more robust — closer to the true line despite outliers.')

L2 is pulled toward the outliers (sensitive to large errors).

L1 is more robust — closer to the true line despite outliers.

VIII. Physics Applications#

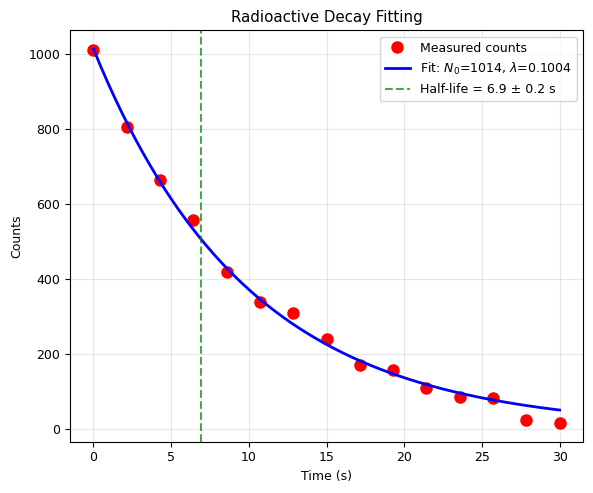

1. Radioactive Decay#

Radioactive decay follows: \(N(t) = N_0 \, e^{-\lambda t}\)

where \(\lambda\) is the decay constant and \(t_{1/2} = \ln 2 / \lambda\).

# Radioactive decay fitting

def decay_model(t, N0, lam):

return N0 * np.exp(-lam * t)

# Simulate "experimental" data

np.random.seed(42)

N0_true, lam_true = 1000, 0.1 # True parameters

t_data = np.linspace(0, 30, 15)

N_data = decay_model(t_data, N0_true, lam_true) + 20 * np.random.randn(15)

N_data = np.maximum(N_data, 0) # Can't have negative counts

# Fit

params_decay, cov_decay = curve_fit(decay_model, t_data, N_data, p0=[800, 0.05])

N0_fit, lam_fit = params_decay

errs_decay = np.sqrt(np.diag(cov_decay))

# Calculate half-life

half_life = np.log(2) / lam_fit

half_life_err = np.log(2) / lam_fit**2 * errs_decay[1] # Error propagation

# Plot

t_fine = np.linspace(0, 30, 200)

plt.figure(figsize=(6, 5))

plt.plot(t_data, N_data, 'ro', markersize=8, label='Measured counts')

plt.plot(t_fine, decay_model(t_fine, *params_decay), 'b-', linewidth=2,

label=f'Fit: $N_0$={N0_fit:.0f}, $\\lambda$={lam_fit:.4f}')

plt.axvline(half_life, color='g', linestyle='--', alpha=0.7,

label=f'Half-life = {half_life:.1f} ± {half_life_err:.1f} s')

plt.xlabel('Time (s)')

plt.ylabel('Counts')

plt.title('Radioactive Decay Fitting')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f'True: N0 = {N0_true}, lambda = {lam_true}, half-life = {np.log(2)/lam_true:.2f} s')

print(f'Fitted: N0 = {N0_fit:.1f} +/- {errs_decay[0]:.1f}')

print(f' lambda = {lam_fit:.4f} +/- {errs_decay[1]:.4f}')

print(f' half-life = {half_life:.2f} +/- {half_life_err:.2f} s')

True: N0 = 1000, lambda = 0.1, half-life = 6.93 s

Fitted: N0 = 1013.6 +/- 15.2

lambda = 0.1004 +/- 0.0024

half-life = 6.91 +/- 0.17 s

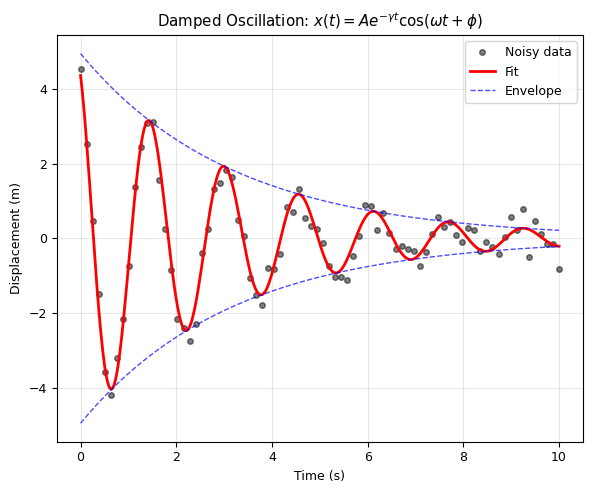

2. Damped Oscillation#

A damped oscillator: \(x(t) = A \, e^{-\gamma t} \cos(\omega t + \phi)\)

# Damped oscillation fitting

def damped_oscillation(t, A, gamma, omega, phi):

return A * np.exp(-gamma * t) * np.cos(omega * t + phi)

# Simulate data

np.random.seed(42)

A_true, gamma_true, omega_true, phi_true = 5.0, 0.3, 4.0, 0.5

t_osc = np.linspace(0, 10, 80)

x_osc = damped_oscillation(t_osc, A_true, gamma_true, omega_true, phi_true)

x_osc_noisy = x_osc + 0.3 * np.random.randn(len(t_osc))

# Fit

params_osc, cov_osc = curve_fit(damped_oscillation, t_osc, x_osc_noisy,

p0=[4, 0.2, 3.5, 0])

A_fit, gamma_fit, omega_fit, phi_fit = params_osc

# Plot

t_fine = np.linspace(0, 10, 500)

plt.figure(figsize=(6, 5))

plt.plot(t_osc, x_osc_noisy, 'ko', markersize=4, alpha=0.5, label='Noisy data')

plt.plot(t_fine, damped_oscillation(t_fine, *params_osc), 'r-', linewidth=2, label='Fit')

plt.plot(t_fine, A_fit * np.exp(-gamma_fit * t_fine), 'b--', linewidth=1,

alpha=0.7, label='Envelope')

plt.plot(t_fine, -A_fit * np.exp(-gamma_fit * t_fine), 'b--', linewidth=1, alpha=0.7)

plt.xlabel('Time (s)')

plt.ylabel('Displacement (m)')

plt.title(r'Damped Oscillation: $x(t) = A e^{-\gamma t} \cos(\omega t + \phi)$')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f'Fitted parameters:')

print(f' Amplitude A = {A_fit:.3f} (true: {A_true})')

print(f' Damping gamma = {gamma_fit:.3f} s^-1 (true: {gamma_true})')

print(f' Frequency omega = {omega_fit:.3f} rad/s (true: {omega_true})')

print(f' Phase phi = {phi_fit:.3f} rad (true: {phi_true})')

print(f'\n Quality factor Q = omega/(2*gamma) = {omega_fit/(2*gamma_fit):.2f}')

Fitted parameters:

Amplitude A = 4.941 (true: 5.0)

Damping gamma = 0.314 s^-1 (true: 0.3)

Frequency omega = 4.014 rad/s (true: 4.0)

Phase phi = 0.493 rad (true: 0.5)

Quality factor Q = omega/(2*gamma) = 6.40

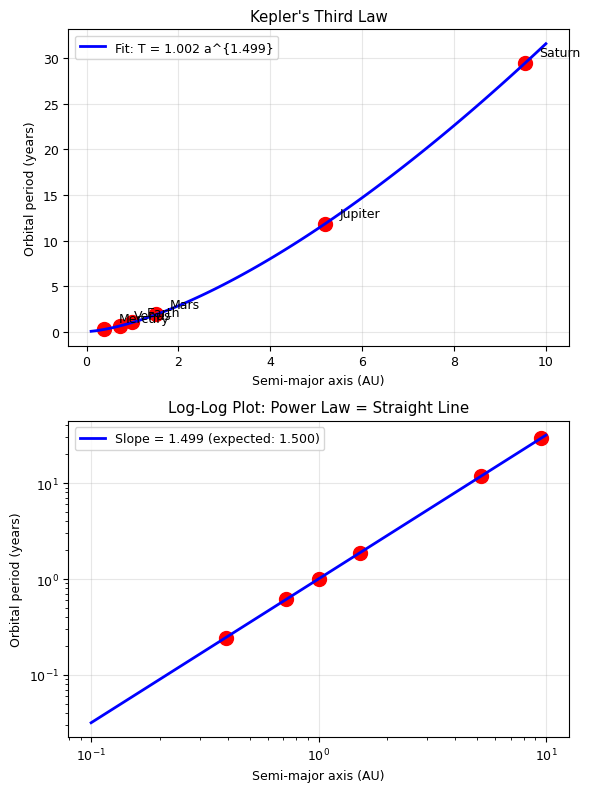

3. Power Law: Kepler’s Third Law#

Kepler’s Third Law: \(T^2 = a^3\) (in appropriate units)

Or equivalently: \(T = C \cdot a^{3/2}\), which is a power law!

# Kepler's Third Law

def power_law(x, C, n):

return C * x**n

# Planetary data

planet_names = ['Mercury', 'Venus', 'Earth', 'Mars', 'Jupiter', 'Saturn']

a_AU = np.array([0.39, 0.72, 1.00, 1.52, 5.20, 9.54]) # Semi-major axis (AU)

T_yr = np.array([0.24, 0.62, 1.00, 1.88, 11.86, 29.46]) # Period (years)

# Fit power law T = C * a^n

params_kepler, cov_kepler = curve_fit(power_law, a_AU, T_yr, p0=[1, 1.5])

C_fit, n_fit = params_kepler

errs_kepler = np.sqrt(np.diag(cov_kepler))

fig, axes = plt.subplots(2, 1, figsize=(6, 8))

# Linear plot

a_fine = np.linspace(0.1, 10, 100)

axes[0].plot(a_AU, T_yr, 'ro', markersize=10)

for i, name in enumerate(planet_names):

axes[0].annotate(name, (a_AU[i], T_yr[i]), textcoords='offset points',

xytext=(10, 5), fontsize=9)

axes[0].plot(a_fine, power_law(a_fine, *params_kepler), 'b-', linewidth=2,

label=f'Fit: T = {C_fit:.3f} a^{{{n_fit:.3f}}}')

axes[0].set_xlabel('Semi-major axis (AU)')

axes[0].set_ylabel('Orbital period (years)')

axes[0].set_title("Kepler's Third Law")

axes[0].legend()

axes[0].grid(True, alpha=0.3)

# Log-log plot (power law becomes a straight line!)

axes[1].loglog(a_AU, T_yr, 'ro', markersize=10)

axes[1].loglog(a_fine, power_law(a_fine, *params_kepler), 'b-', linewidth=2,

label=f'Slope = {n_fit:.3f} (expected: 1.500)')

axes[1].set_xlabel('Semi-major axis (AU)')

axes[1].set_ylabel('Orbital period (years)')

axes[1].set_title('Log-Log Plot: Power Law = Straight Line')

axes[1].legend()

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Fitted: T = {C_fit:.4f} * a^{n_fit:.4f}")

print(f"Expected (Kepler): T = 1.000 * a^1.500")

print(f"\nFitted exponent: {n_fit:.4f} +/- {errs_kepler[1]:.4f}")

print(f"Deviation from 3/2: {abs(n_fit - 1.5):.4f}")

print(f"\nKepler's Third Law confirmed!")

Fitted: T = 1.0020 * a^1.4990

Expected (Kepler): T = 1.000 * a^1.500

Fitted exponent: 1.4990 +/- 0.0006

Deviation from 3/2: 0.0010

Kepler's Third Law confirmed!

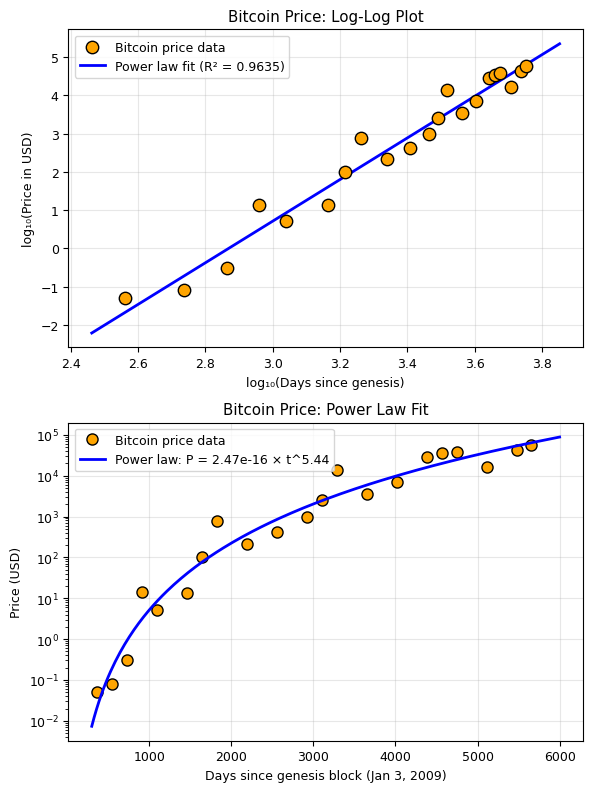

4. Econophysics: Bitcoin Power Law#

Econophysics applies methods from statistical physics to financial systems. It’s a recognized branch of physics studied at institutions worldwide since the 1990s.

Power laws appear throughout econophysics:

Wealth distribution (Pareto’s Law)

Price return distributions (fat tails)

Network growth effects (Metcalfe’s Law)

A remarkable empirical observation: Bitcoin’s price appears to follow a power law in time:

where \(t\) is time (days since Bitcoin’s creation). On a log-log plot, this should appear as a straight line.

Key question: Is this a fundamental “law” like Kepler’s, or just an empirical trend?

# Econophysics: Bitcoin Power Law Fitting

# Historical Bitcoin price data (monthly averages, selected points)

# Source: publicly available Bitcoin price history

# Days since Bitcoin genesis block (Jan 3, 2009)

# Selected data points spanning 2010-2024

btc_days = np.array([

365, # Jan 2010

545, # Jul 2010

730, # Jan 2011

912, # Jul 2011

1095, # Jan 2012

1460, # Jan 2013

1642, # Jul 2013

1825, # Jan 2014

2190, # Jan 2015

2555, # Jan 2016

2920, # Jan 2017

3100, # Jul 2017

3285, # Jan 2018

3650, # Jan 2019

4015, # Jan 2020

4380, # Jan 2021

4562, # Jul 2021

4745, # Jan 2022

5110, # Jan 2023

5475, # Jan 2024

5650, # Jul 2024

])

# Approximate price (USD) at those dates

btc_price = np.array([

0.05, # Jan 2010

0.08, # Jul 2010

0.30, # Jan 2011

14.0, # Jul 2011

5.3, # Jan 2012

13.3, # Jan 2013

100.0, # Jul 2013

770.0, # Jan 2014

215.0, # Jan 2015

430.0, # Jan 2016

960.0, # Jan 2017

2500.0, # Jul 2017

13400.0, # Jan 2018

3500.0, # Jan 2019

7200.0, # Jan 2020

29000.0, # Jan 2021

35000.0, # Jul 2021

38500.0, # Jan 2022

16500.0, # Jan 2023

42000.0, # Jan 2024

57000.0, # Jul 2024

])

# Fit power law: P = a * t^n

# Use log-log linearization for robustness

log_days = np.log10(btc_days)

log_price = np.log10(btc_price)

# Linear fit in log-log space: log(P) = log(a) + n*log(t)

p_btc = np.polyfit(log_days, log_price, 1)

n_btc = p_btc[0]

a_btc = 10**p_btc[1]

# Also fit directly with curve_fit

def power_law(x, a, n):

return a * x**n

params_btc, cov_btc = curve_fit(power_law, btc_days, btc_price,

p0=[1e-10, 5], maxfev=10000)

a_btc_cf, n_btc_cf = params_btc

# R² in log space

r2_btc = compute_r_squared(log_price, np.polyval(p_btc, log_days))

fig, axes = plt.subplots(2, 1, figsize=(6, 8))

# Log-log plot

axes[0].scatter(log_days, log_price, c='orange', s=80, edgecolors='black',

linewidths=1, zorder=5, label='Bitcoin price data')

log_days_fine = np.linspace(np.min(log_days) - 0.1, np.max(log_days) + 0.1, 100)

axes[0].plot(log_days_fine, np.polyval(p_btc, log_days_fine), 'b-', linewidth=2,

label=f'Power law fit (R² = {r2_btc:.4f})')

axes[0].set_xlabel('log₁₀(Days since genesis)')

axes[0].set_ylabel('log₁₀(Price in USD)')

axes[0].set_title('Bitcoin Price: Log-Log Plot')

axes[0].legend()

axes[0].grid(True, alpha=0.3)

# Regular scale with fit

days_fine = np.linspace(300, 6000, 200)

axes[1].semilogy(btc_days, btc_price, 'o', color='orange', markersize=8,

markeredgecolor='black', label='Bitcoin price data')

axes[1].semilogy(days_fine, a_btc * days_fine**n_btc, 'b-', linewidth=2,

label=f'Power law: P = {a_btc:.2e} × t^{n_btc:.2f}')

axes[1].set_xlabel('Days since genesis block (Jan 3, 2009)')

axes[1].set_ylabel('Price (USD)')

axes[1].set_title('Bitcoin Price: Power Law Fit')

axes[1].legend()

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f'Power law fit (log-log linear regression):')

print(f' P(t) = {a_btc:.2e} × t^{n_btc:.2f}')

print(f' Exponent n = {n_btc:.3f}')

print(f' R² (in log space) = {r2_btc:.4f}')

print(f'\nPower law fit (direct curve_fit):')

print(f' P(t) = {a_btc_cf:.2e} × t^{n_btc_cf:.2f}')

Power law fit (log-log linear regression):

P(t) = 2.47e-16 × t^5.44

Exponent n = 5.440

R² (in log space) = 0.9635

Power law fit (direct curve_fit):

P(t) = 1.59e-09 × t^3.60

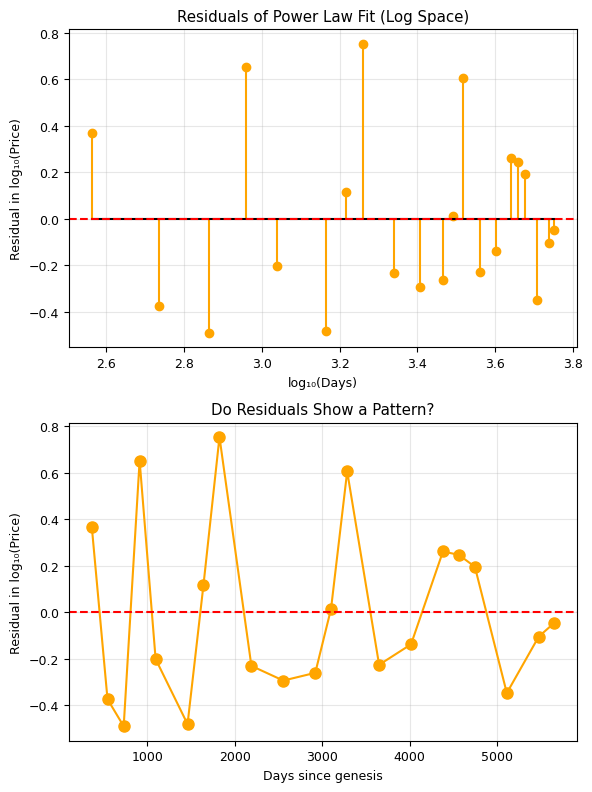

# Critical analysis: examine the residuals in log space

residuals_btc = log_price - np.polyval(p_btc, log_days)

fig, axes = plt.subplots(2, 1, figsize=(6, 8))

# Residuals

axes[0].stem(log_days, residuals_btc, linefmt='orange', markerfmt='o', basefmt='k-')

axes[0].axhline(0, color='r', linestyle='--')

axes[0].set_xlabel('log₁₀(Days)')

axes[0].set_ylabel('Residual in log₁₀(Price)')

axes[0].set_title('Residuals of Power Law Fit (Log Space)')

axes[0].grid(True, alpha=0.3)

# Residuals vs time to check for patterns

axes[1].plot(btc_days, residuals_btc, 'o-', color='orange', markersize=8)

axes[1].axhline(0, color='r', linestyle='--')

axes[1].set_xlabel('Days since genesis')

axes[1].set_ylabel('Residual in log₁₀(Price)')

axes[1].set_title('Do Residuals Show a Pattern?')

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print('Discussion questions:')

print('1. Do the residuals look random, or is there a pattern (e.g., cycles)?')

print('2. The oscillations around the power law may relate to Bitcoin halving cycles (~4 years)')

print('3. How is this different from Kepler\'s Third Law?')

print(' - Kepler: derived from fundamental physics (gravity)')

print(' - Bitcoin: empirical observation from a complex system (no first-principles derivation)')

print('4. Can we use this fit to PREDICT future prices? Why or why not?')

print('5. What would falsify the power law model?')

Discussion questions:

1. Do the residuals look random, or is there a pattern (e.g., cycles)?

2. The oscillations around the power law may relate to Bitcoin halving cycles (~4 years)

3. How is this different from Kepler's Third Law?

- Kepler: derived from fundamental physics (gravity)

- Bitcoin: empirical observation from a complex system (no first-principles derivation)

4. Can we use this fit to PREDICT future prices? Why or why not?

5. What would falsify the power law model?

IX. Advanced Topics (Brief Overview)#

Maximum Likelihood Estimation (MLE)#

Finds parameters that maximize the probability of observing the data. For Gaussian noise, MLE is equivalent to least squares!

Bayesian Fitting#

Uses Bayes’ theorem to compute the posterior probability distribution of parameters:

This gives not just the best parameters, but their full probability distribution!

Weighted Least Squares#

When data points have different uncertainties \(\sigma_i\):

Points with smaller error bars contribute more to the fit.

# Weighted vs unweighted fitting

np.random.seed(42)

x_w = np.linspace(0, 5, 15)

y_true_w = 2 * x_w + 1

# Different uncertainties: first few points very precise, last few noisy

sigma_w = np.concatenate([0.1 * np.ones(8), 2.0 * np.ones(7)])

y_w = y_true_w + sigma_w * np.random.randn(15)

# Unweighted fit

p_unw = np.polyfit(x_w, y_w, 1)

# Weighted fit

p_weighted = np.polyfit(x_w, y_w, 1, w=1/sigma_w)

plt.figure(figsize=(6, 5))

plt.errorbar(x_w, y_w, yerr=sigma_w, fmt='ko', markersize=6, capsize=5, label='Data')

plt.plot(x_w, np.polyval(p_unw, x_w), 'b-', linewidth=2,

label=f'Unweighted: y = {p_unw[0]:.2f}x + {p_unw[1]:.2f}')

plt.plot(x_w, np.polyval(p_weighted, x_w), 'r--', linewidth=2,

label=f'Weighted: y = {p_weighted[0]:.2f}x + {p_weighted[1]:.2f}')

plt.plot(x_w, y_true_w, 'g:', linewidth=2, label='True: y = 2x + 1')

plt.xlabel('x')

plt.ylabel('y')

plt.title('Weighted vs Unweighted Fitting')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print('Weighted fit trusts precise points more -> closer to true line!')